Rapidan Energy Group, an energy market, policy and geopolitical data and research firm based in Washington, DC and Houston, TX, has released its proprietary data and analysis on the Gulf War III oil supply disruption and the impact of Gulf War III on global oil markets. The firm was founded and headed by Bob McNally, a former White House energy advisor to President George W. Bush and author of the award-winning book Crude Volatility: The History and the Future of Boom-Bust Oil Prices (Columbia University Press, 2017).

Key Findings

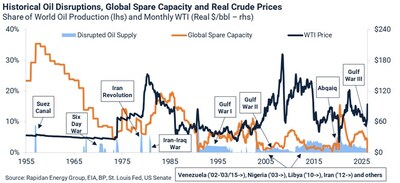

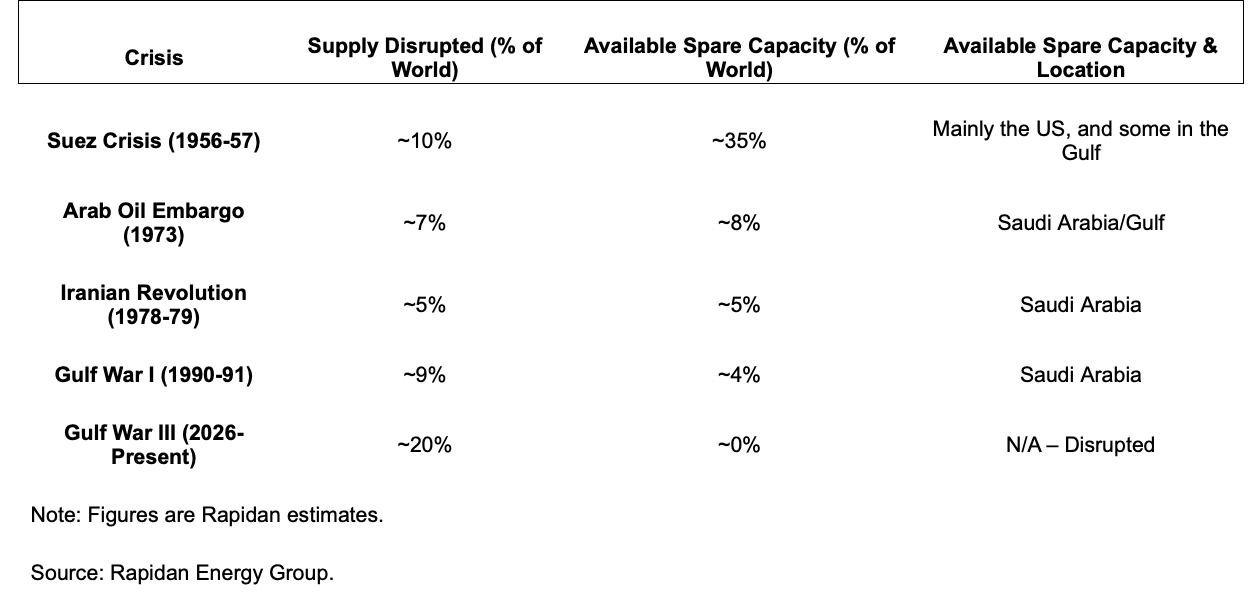

- Gulf War III has disrupted ~20% of global oil supply for nine days and counting – more than double the previous record set during the Suez Crisis of 1956-57, which disrupted just under 10%.

- This is not a demand shock. It is a simultaneous supply and buffer shock: the conflict has disrupted both production flows and the spare capacity that markets rely upon to offset disruptions.

- The primary holders of spare capacity – Saudi Arabia and the UAE – have been cut off from global oil markets, effectively eliminating the industry's traditional shock absorber.

- During the Suez Crisis – the last time a disruption approached this scale – spare capacity stood at ~35% of global supply and was located largely in the US, where it was available to global markets. That cushion no longer exists.

- Absent a near-term resumption of Strait of Hormuz flows, the global oil market will need to balance via demand destruction caused by sharply rising oil prices.

The Historical Record: Why This Time is Different

Rapidan Energy Group's proprietary historical disruption dataset – covering every major supply event since 1950 – confirms that Gulf War III has exceeded any prior disruption by more than 2x.

The Spare Capacity Problem – The Shock Absorber is Gone

Available spare production capacity has mitigated every major oil disruption in the post-war era, to varying degrees. In 1956-57, the US and international majors held spare capacity equivalent to ~35% of world supply. During the 1973 Arab Oil Embargo and subsequent Gulf crises, Saudi Arabia and Gulf producers maintained several million barrels per day of swing capacity.

Gulf War III has changed this calculus entirely. The conflict has not only taken offline a historically high share of global supply – it has simultaneously disrupted the primary holders of spare capacity. The disruption zone directly implicates Saudi Arabia and the UAE, which collectively accounted for the overwhelming majority of the world's available pre-war buffer.

The result is a market with no meaningful cushion. There is no swing producer positioned to step in. The standard framework for oil disruption analysis – assess the disruption, identify spare capacity offsets, model a recovery path – does not apply here.

Oil Market Implications — Gulf War III Oil Supply Disruption

- Price formation is now operating without the backstop that has traditionally imposed a price ceiling. In prior disruptions, spare capacity constrained price upside by providing a credible supply response. That mechanism is absent.

- IEA members will come under intense pressure to release strategic stocks – the only remaining supply response option. But Strategic Petroleum Reserve (SPR) releases are finite and insufficient to fully offset the Hormuz loss.

- Demand destruction and fuel switching will serve as the primary market-clearing mechanism in the absence of supply-side relief, as consumers and industries adjust their consumption patterns in response to higher prices and limited fuel availability.