For the past year, Rusty Braziel, founder and executive chairman of RBN Energy (located in Houston, Texas), has correctly warned BPN readers about the challenges presented by the ever-increasing exporting of United States propane. In a blog dated July 7, 2021, “Skyrockets in Flight — Propane Headed Toward Uncharted Territory,” Braziel presented the backstory on how U.S. propane surpluses have eroded in recent years amid modest production growth but near record-high export volumes. Here are some excerpts:

“Fourth of July skyrockets were not the only fireworks earlier this week. The price of propane skyrocketed up to 112 c/gal before the holiday weekend and held at that level through Tuesday, an increase of about 21 c/gal or 23% over the past month alone. To put that in perspective, that’s the highest price for propane since April 2014, back when crude oil was over $100/bbl. Although propane came off a few cents on Wednesday in sympathy with falling crude prices, both Mont Belvieu and Conway propane prices are still almost 135% higher than this time last year.

“Fourth of July skyrockets were not the only fireworks earlier this week. The price of propane skyrocketed up to 112 c/gal before the holiday weekend and held at that level through Tuesday, an increase of about 21 c/gal or 23% over the past month alone. To put that in perspective, that’s the highest price for propane since April 2014, back when crude oil was over $100/bbl. Although propane came off a few cents on Wednesday in sympathy with falling crude prices, both Mont Belvieu and Conway propane prices are still almost 135% higher than this time last year.

Assuming crude prices don’t fall off a cliff, how high could propane prices go? Hard to say. The propane market is experiencing unusually low inventories, relatively modest production growth, near record-high export volumes, and unconstrained dock capacity. Consequently, if we continue to see strong demand, but U.S. producers stay focused on capital discipline, thus constraining production, propane prices could be considerably higher this winter.

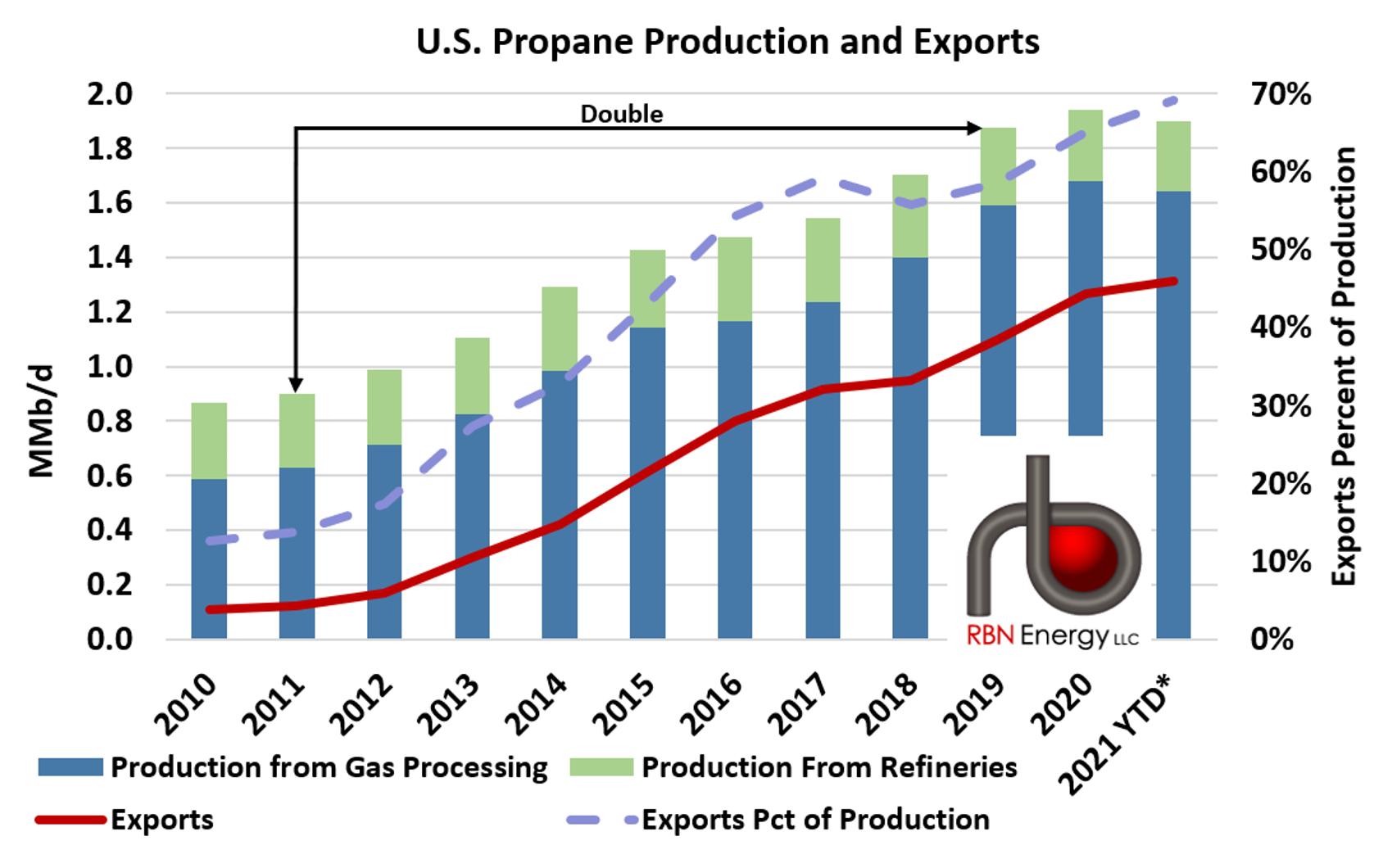

“We’ve been worrying about propane on a regular basis for over a year now, and it’s all about exports. Here’s the backstory. Most propane is a byproduct of oil and gas production (blue bar segments and left axis in Figure 1), with a smaller volume a byproduct of oil refining (green bar segments). Years ago, as the Shale Revolution was kicking in, the production of propane ramped up, with volumes doubling between 2011 and 2019 (black arrows labeled “Double”). But propane demand in the U.S. consumer (retail, etc.) and petrochemical sectors was flat, so there was only one way to balance the market: exports (red line and left axis). The problem was, in the early days of shale-driven propane production growth, U.S. dock capacity was insufficient to export all of the surplus, and international demand was only experiencing modest growth. The result was restrained exports. That pushed U.S. propane prices into the doghouse. For the next five years, propane production tended to stay ahead of international demand and export dock capacity, resulting in surplus market conditions most of the time. U.S. propane consumers — everyone from backyard BBQ-ers to huge petrochemical plants — enjoyed cheap propane, for a while.

“We’ve been worrying about propane on a regular basis for over a year now, and it’s all about exports. Here’s the backstory. Most propane is a byproduct of oil and gas production (blue bar segments and left axis in Figure 1), with a smaller volume a byproduct of oil refining (green bar segments). Years ago, as the Shale Revolution was kicking in, the production of propane ramped up, with volumes doubling between 2011 and 2019 (black arrows labeled “Double”). But propane demand in the U.S. consumer (retail, etc.) and petrochemical sectors was flat, so there was only one way to balance the market: exports (red line and left axis). The problem was, in the early days of shale-driven propane production growth, U.S. dock capacity was insufficient to export all of the surplus, and international demand was only experiencing modest growth. The result was restrained exports. That pushed U.S. propane prices into the doghouse. For the next five years, propane production tended to stay ahead of international demand and export dock capacity, resulting in surplus market conditions most of the time. U.S. propane consumers — everyone from backyard BBQ-ers to huge petrochemical plants — enjoyed cheap propane, for a while.

“Then the market responded — just as you might expect. International buyers — especially in Asia — expanded plants to use a lot more U.S. propane, and midstream companies built out more U.S. dock capacity to enable additional exports. By the end of the 2010s, it looked like U.S. propane markets were headed toward tight market conditions, with U.S. demand competing head-to-head with exports, which by then accounted for about 60% of the demand for U.S. production (dashed light blue line and right axis in Figure 1). But then COVID happened, and that put the looming supply/demand imbalance in limbo. Propane production fell off along with crude, natural gas, and NGLs. Petchems cut back on propane purchases. Already bulging inventories increased toward record highs. And export volumes dropped, but not for long.

“In very short order, exports returned to pre-COVID levels. That was the canary in the coal mine — the first signal that trouble was coming. Propane exports seemed to be relatively impervious to the COVID disruptions that continued to roil other energy markets during 2020.

By mid-year the implications were clear: Constraints on exports — both on the supply end with U.S. dock capacity and the demand end with international requirements — had been relieved. As we’ve stated in several blogs, most recently in “Higher,” now the only way U.S. propane inventories can be built back up in the summer/fall seasons to ensure adequate stocks to meet winter season demand is for U.S. propane prices to get so high that export cargoes get canceled, effectively keeping those barrels in U.S. storage.”

Where Is the Market Headed?

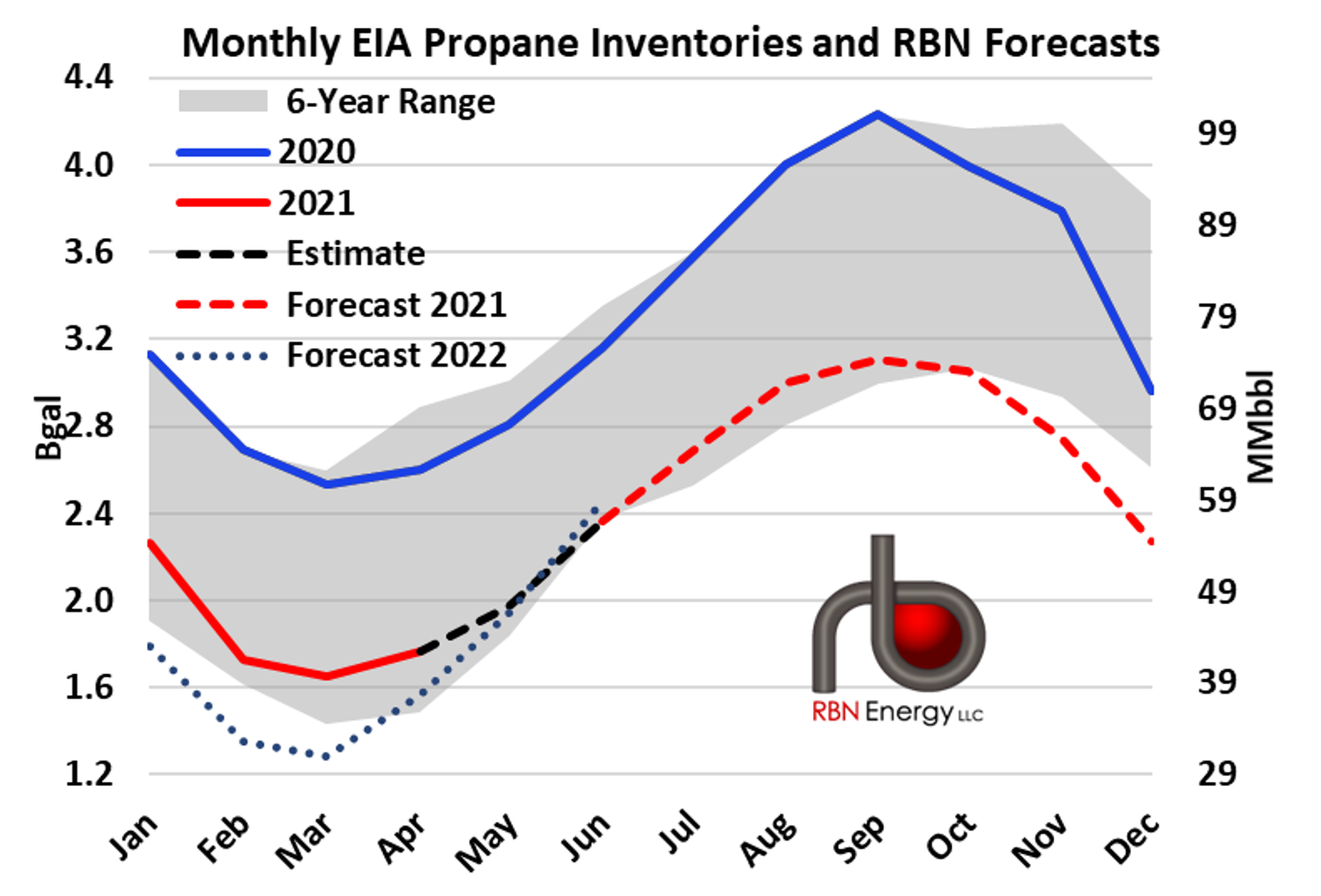

“Fast-forward to July 2021. Propane exports are still running high, and production is up, but only slightly,” Braziel said. “As a result, stocks have not been replenished at a rate necessary for the market to be comfortable by the onset of winter season demand. Figure 2 lays out RBN’s assessment of propane stocks over the next 12 months in the context of historical trends, showing propane inventories last year (blue line), the six-year monthly high-low range (gray area), actual EIA monthly inventories for 2021 through April (red line), RBN’s estimate of inventories in May and June based on EIA weekly data (dashed black line), our forecast for the balance of this year (dashed red line) and finally our forecast for the first six months of next year (dotted blue line).”

Noting there is a lot of information, he said these are the main takeaways:

- Inventories have been scraping along the bottom of the six-year inventory range and have been running about 20 million barrels (850 million gallons) below last year.

- June inventories rose by about 9.3 MMbbl (391 MM gallons) to 56.3 MMbbl (2.4 billion gallons), which is about 200 Mbbl below the five-year minimum.

- Over the next four months, inventories will build to levels slightly above the six-year minimum, but that will not be enough to keep stocks from falling below the minimum for the November 2021 through March 2022 period.

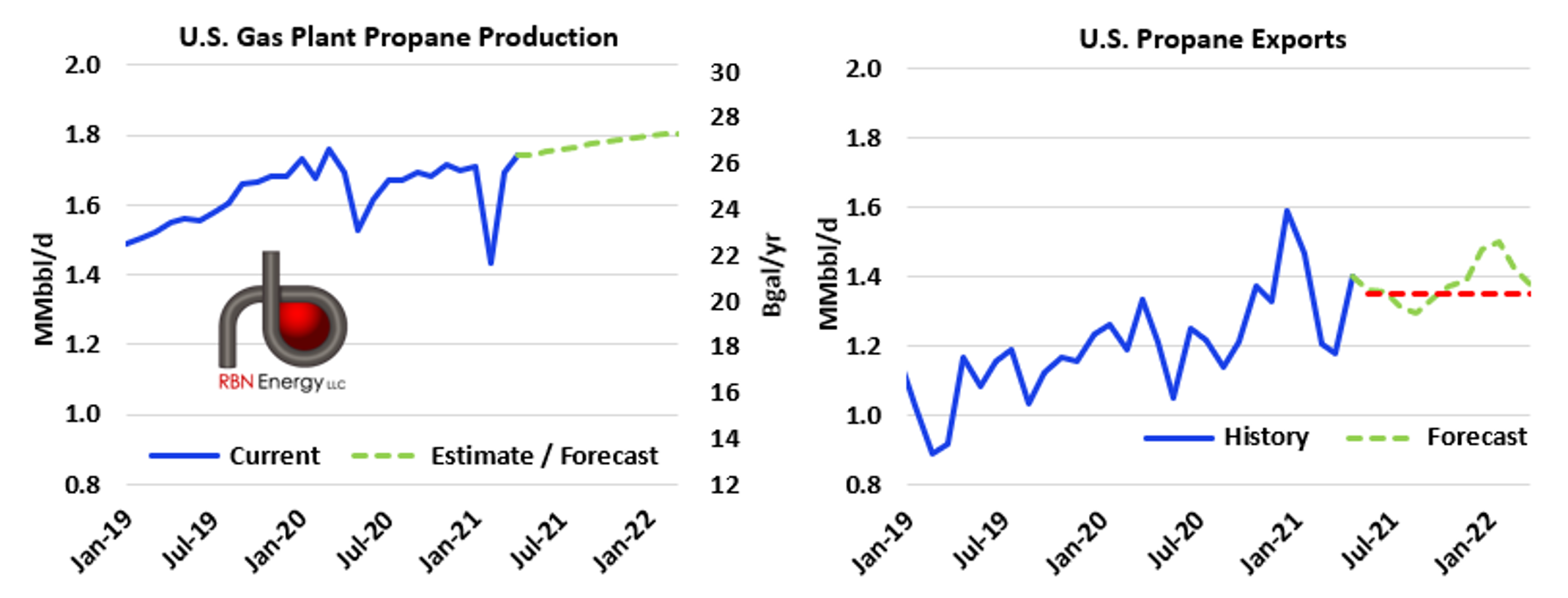

“Of course, in the calculations necessary to develop the graphic in Figure 2, many premises must be set and assumptions made,” Braziel said. “Two of the most important of these are shown in Figure 3. The left graph indicates that U.S. propane production from gas processing has been increasing gradually since the COVID-19 meltdown in the spring of 2020, interrupted by February 2021’s deep freeze. Over the year, production is up about 8%, recovering to pre-COVID levels in April. We expect that the rate of propane production growth will slow over the coming months, but still come in with about a 3% increase over the next year (dashed green line).

“The more significant assumption is in our assessment of propane exports,” he said. “Based on our forecasts, propane exports will continue at an average of about 1.35 MMb/d (dashed red line in right graph), which is only slightly higher than where exports have been since mid-2020 after the meltdown, other than a blip lower during February’s deep freeze.” He noted this assessment assumes that exports will be constrained by high propane prices in the U.S. compared to prices in Asia, resulting in the cancellation of some cargoes.

“However, note that we do expect an increase in exports during the early part of winter 2021-2022 (peak in dashed green line) as seasonal Asia demand pulls in more barrels, regardless of price,” Braziel said. “It is during this period when U.S. markets are likely to be particularly exposed to very high prices, especially if cold weather in the U.S. were to coincide with cold weather in Asia. If things play out that way, it would be truly uncharted territory for propane markets.”

Braziel and his team at RBN Energy are responding to the increased market concerns with a new weekly publication, “U.S. Propane Market Update & Outlook.”

More Supply Factors to Consider

“Inventory and days of supply — these two items have been the focal point of most fundamental propane analysis for years,” said J.D. Buss, trading and risk management advisor at Twin Feathers (located in Overland Park, Kansas). “They remain viable analytical tools, but they need three things added into the mix to provide an accurate picture.”

He described the first and foremost need as the status of U.S. propane exports. “Over the last decade, propane exports have outstripped domestic U.S. demand. Calendar year 2021 is already on pace to set another export volume record. Looking into the future, U.S. propane prices continue to be supportive through calendar year 2022. And most importantly, U.S. propane prices remain one of the lowest (if not the lowest) value, which will continue to support propane export growth.”

Buss noted that propane production has been on an uphill climb for the last decade. “However, the first half of 2021 has seen production rates that are steady and holding in a narrow range. Going back a year, many thought propane production would be 2.4 million bbls or more per day. Yet current values stand at 2.3 million bbls per day. Not having a possible 100,000 bbls per day for half a year generates an inventory deficit of 18 million bbls. Something to consider as we move forward through 2021.”

A final item to consider according to Buss: an inventory reality check. What does he mean by that? “Belvieu (Gulf Coast inventory) will most likely be used for exports, not the domestic U.S. market. Conway inventory, which in prior decades has been the major Midwest reserve, could merely be a holding location for Gulf Coast exports.”

He believes days of supply available is important data to review, but it may be more vital to look at that stat on a regional basis. “Total inventory available will always be a telltale indicator for prices but … regional U.S. prices may be more informative and predictive as a retailer moves through winter.”

Buss has been working with his clients at Twin Feathers to add the new dimensions and data points to the factors they are taking into account when making supply decisions.

Anne Keller, managing director at Midstream Energy Group, noted there were concerns about supply tightness last winter, especially in outlying areas, because production in regions outside Texas was slowing dramatically and the Chinese tariff on imported propane was lifted in March 2020.

“Removing the 25% tariff immediately kicked off an increase in exports to China that largely offset the falloff in domestic demand,” Keller said. “One of the unheralded but very important issues for those who need to understand the propane markets is that the EIA is only charged with tracking the portion of the hydrocarbon market that is considered to be part of the energy space. But nearly 50% of U.S. NGL production, including basically all the ethane, goes into the petrochemical market. The inventory statistics we see in the EIA reports only include barrels in commercial storage and at refineries, which are considered available to the ‘energy’ portion of the hydrocarbon market. Inventory held by chemicals is not surveyed since it’s considered to be a raw material for manufacturing.”

Keller said the industry has recently seen bumps in inventory in the Gulf Coast, which are not all due to the cancellation of cargoes. “Some of these represent transfers from chemical storage back into commercial facilities. This isn’t new supply; it’s just shuffling the barrels we have.”

“With propylene prices as strong as they are and six new on-purpose propylene units due to start up in China this year, it’s not hard to imagine a ‘coyote moment’ for the market in the not-too-distant future where prices really spike,” Keller said. “The ‘Product Supplied’ number that’s shown in Energy Information Administration balances doesn’t represent the total market, but a lot of people assume that it somehow does represent total domestic demand.”

She said that with cargoes gobbling up 500,000-600,000 barrels at a time, and limited insight on where total inventory balances really are here on the Gulf Coast, just a few liftings can really change the picture. “Basically, we’ve finally rebalanced the U.S. market to the point it was before the shale boom, where propane trades in a range closer to its Btu value versus crude again. Only now we have customers overseas who have converted to LPG to take advantage of its cleaner-burning, more environmentally-friendly properties. And their governments can step in to subsidize some of the cost if the market is tight. That’s not the case in the U.S.”

Preparing for Winter in the U.S. Southeast

“Despite having to work through COVID restrictions and limitations, 2020-2021 was a banner year in the Southeast, with low prices, consistently cool weather and minimal supply or transportation issues,” said Phil Farris, director of wholesale marketing at 3Eight Energy, (Danvers, North Carolina.) “This year presents more of a challenge.”

“As of early July, U.S. propane and propylene stocks are down about 20% from last year, and just barely within the five-year range,” Farris said. “Gulf Coast (PADD 3) inventories, which affect most of the Southeast market, are in a similar state. A strong spring/early summer commodity market, driven by economic recovery, crude oil and the production-export-inventory equation, has put prices about 30% over the 10-year average for Mont Belvieu propane. Depending on who you talk to and their objective, there are varying degrees of concern regarding inventory levels and market conditions. With Southeast retail demand at seasonal lows, the focus is on summer and fall agriculture demand, which looks strong as of early July. The current ‘higher than everyone wants’ value for propane doesn’t feel too good to retailers. But it does help the overall cause by possibly keeping a lid on additional exports, thus boosting inventory before winter.”

Regarding a late 2021 outlook and potential issues, Farris said that for now PADD 3 inventory levels are worth watching, but shares the concern of others about the data so far to suggest how serious a storage or major issue may be regarding retail winter demand.

“Transportation will continue to be a question and discussion topic,” Farris said. “Plenty of trucks — but finding and juggling drivers and lobbying for HOS relief will keep dispatchers up late. One thing everyone agrees on: ‘Relative to normal’ and ‘Compared to last year’ are not the same thing! Most retailers contract or commit to their annual needs in the spring. New business and tank sets can obviously affect a forecast made six months ago.”

Farris encourages marketers to communicate regularly with propane and transportation suppliers, to be active in their state or regional associations and to follow National Propane Gas Association (NPGA) and Propane Education & Research Council (PERC) updates.

NPGA Provides Weekly Supply Updates, Resources for Members

“Over the years, the industry has seen its fair share of stresses on the domestic liquified petroleum gas (LPG) supply and logistics’ infrastructure: hurricanes, polar vortices, rail strikes, freezing/ice events, wet crop harvests, etc.,” said Steve Kossuth, vice president of global LPG supply at UGI Corp. (parent company of AmeriGas). Kossuth also serves as chairman of the National Propane Gas Association’s (NPGA) Propane Supply and Logistics Committee.

“The universal truth remains that stresses on the system are unpredictable,” he said. “While the inputs of stress may be ever-changing, the best practices to combat supply interruptions remain largely unchanged: planning and communication.”

Kossuth said retailers should continue the best practice of considering the type of customers they are supplying, where they are geographically located, taking interest in their supply chains, questioning how their supply and transportation providers are prepared to support their business in the upcoming season and having conversations early and often about planning and execution.

“Considerations of demand, supply, storage, mode of transport (pipeline, rail, truck, length of haul, etc.) and appropriate storage levels are specific to each of our respective businesses. No two businesses are alike,” Kossuth said. “Nobody can predict the future, but education, relationships and communication are the best tools to combat this uncertainty. There is always concern about surety of supply; that is what produces better plans and ironically promotes enhanced surety of supply. The efforts of the excellent people in our industry to navigate change and adapt are remarkable. Suppliers, retailers, pipeline and storage operators, truck drivers, rail crews and terminal operators are all part of this solution.”

“In the wake of the polar vortex, the NPGA had a focused task force produce a white paper of recommendations for retailers to utilize to enhance their surety of supply and increase understanding through education so that informed decisions can take place,” Kossuth said. “I am particularly proud of the work of the NPGA’s Propane Supply and Logistics Committee and the NPGA staff in getting the word out and providing its membership with weekly and monthly supply updates. We have received wonderful feedback on this approach, and retailers, suppliers and transporters have benefited from these efforts.”

He said the industry has also developed its infrastructure since this white paper was produced. “There are more supply points across the United States than in prior years with the development of storage, pipeline, rail and truck infrastructure.”

“The NPGA is working on a webinar to take place late this summer for market fundamentals aimed at reviewing what has happened this summer and what things are looking like from an industry perspective heading into winter,” Kossuth said. “During this same webinar, the NPGA is working on demystifying pipelines, and we will hear from a panel composed of a pipeline operator, a midstream marketer and a retail customer. Better understanding the ecosystem of pipelines and how shipping on these excellent resources works will allow retailers and suppliers to hold better, more informed dialog regarding supply via pipeline. It is the hope of the [Propane Supply and Logistics] Committee that this will lead to better risk assessments and more robust supply planning as we head into this and

future winters.”